April 23, 2026

Most Americans assume their 401(k) gives them access to the best available investments. It doesn’t.

Pension funds and wealthy investors have had access to private markets for decades. The 90 million Americans who depend on a 401(k) have not, thanks to a tangle of regulatory barriers that were never about protecting workers. The result is a two-tiered retirement system: one set of rules for the wealthy and well-connected, and another for everyone else.

The Trump administration is moving to fix that. And the President’s own Council of Economic Advisers just published data showing exactly what American workers have been missing.

A Tale of Two Markets

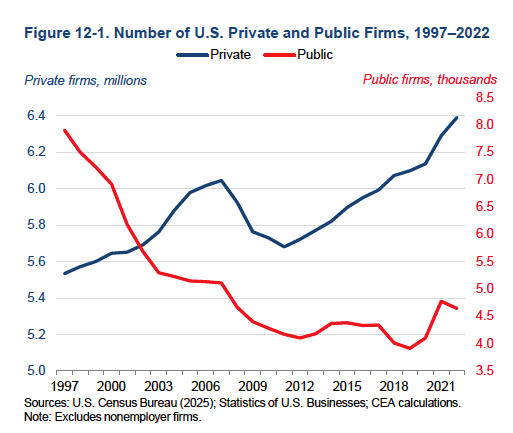

The best investment opportunities increasingly aren’t on any public exchange. The number of public companies has fallen by half since 1997, while private fund assets have surged from $9.5 trillion to $30.9 trillion, more than tripling in just over a decade. The action has moved to private markets. Your 401(k) hasn’t been allowed to follow.

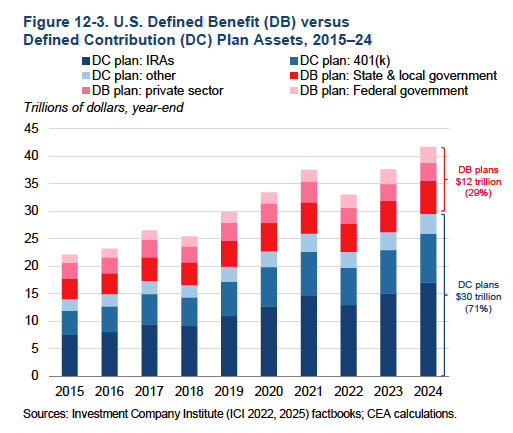

At the same time, the U.S. retirement system has shifted decisively toward defined contribution (DC) plans like 401(k)s. As of 2024, DC plan assets total $30 trillion (roughly 70 percent of all U.S. retirement assets) while traditional pension (defined benefit) plans hold $12 trillion.

Here’s the problem: pension funds, which manage money for teachers, firefighters, and government workers, allocate roughly 30 percent of their portfolios to private markets. 401(k) plans, which cover the vast majority of private-sector workers, allocate just 0.1 percent.

That gap is the product of regulatory barriers: the SEC’s accredited investor rules, which restrict direct access to private investments, and guidance issued by the Biden administration’s Department of Labor in 2021 that discouraged DC plans from offering private market options – effectively telling plan sponsors that doing so was too risky, legally speaking.

The people who got locked out were the 90 million Americans who depend on their 401(k) as their primary retirement vehicle.

What Workers Have Been Missing

Private equity has consistently outperformed public markets. The CEA’s analysis of buyout fund performance finds that PE funds have outperformed the S&P 500 across the vast majority of vintage years, even after accounting for fees.

But the more important question for 401(k) savers isn’t just whether PE beats the stock market. It’s what happens to their actual retirement income when PE is added to their portfolio. The CEA ran the numbers and the results are striking.

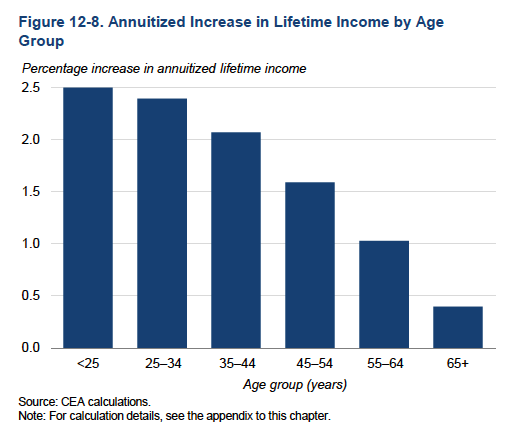

The younger you are, the more you stand to gain. A 25-year-old with access to private equity in their 401(k) could retire with 2.5 percent more lifetime income than someone without it, a meaningful difference compounded over decades of saving. Even workers near retirement see real gains. Across all age groups, the CEA estimates an aggregate 1.3 percent increase in lifetime retirement income.

These figures represent the difference between a more comfortable retirement and a less secure one for tens of millions of Americans.

The Broader Economic Case

The benefits don’t stop at the individual level. The CEA estimates that fully opening 401(k) plans to private equity would lead DC plans to allocate roughly 20 percent of their assets to PE (consistent with what pension funds already do). The resulting shift of capital from lower-productivity public markets to higher-productivity private companies would generate an additional $35 billion in GDP output.

What the Trump Administration Has Done

The path to this moment began on August 7, 2025, when President Trump signed an Executive Order directing the DOL to democratize access to alternative investments for 401(k) savers. DOL quickly followed by rescinding Biden’s 2021 guidance that had been chilling plan sponsor participation.

On March 30, 2026, DOL took the next step, releasing a proposed rule, “Fiduciary Duties in Selecting Designated Investment Alternatives,” that would create a formal safe harbor for plan sponsors who want to offer private market options to their participants. The rule gives fiduciaries a clear process to follow, removing the litigation risk that had kept private equity out of 401(k) plans for years.

The public comment period is open through June 1, 2026. This is the moment for anyone who supports expanding retirement security for working Americans to weigh in.

The data is clear. Pension funds get private equity. Wealthy investors get private equity. The question is simple: why not the 90 million Americans with a 401(k)?

![]()

Subscribe to Pinpoint Policy Institute